Fixed vs Variable APR

Fixed vs Variable APR: understand how each APR type works, how it affects personal loans, monthly payments, borrowing risk, and smarter loan comparison decisions.

Fixed vs Variable APR

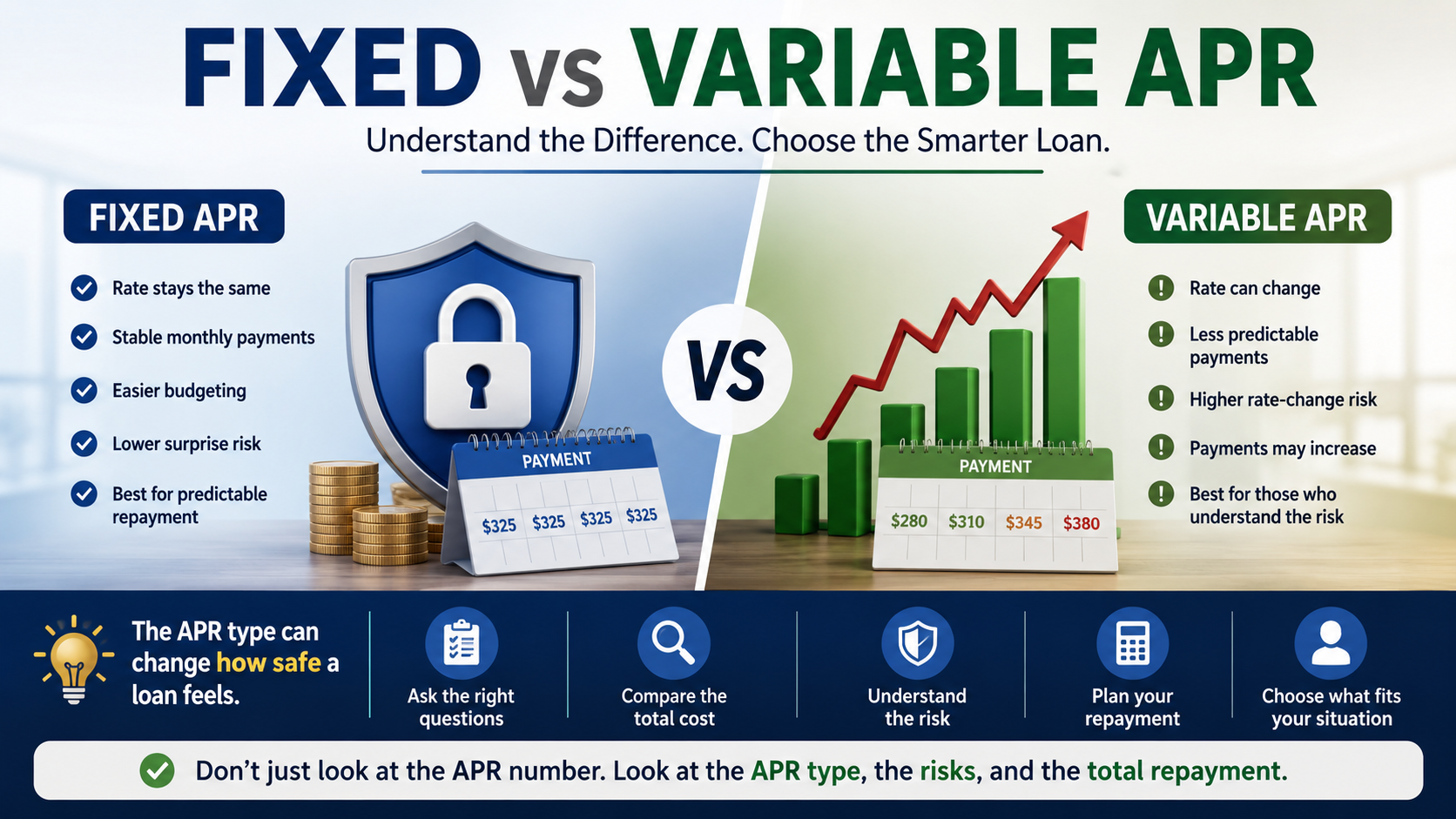

The APR Type Can Change How Safe a Loan Feels

When I compare personal loan offers, I do not look only at the APR number. I also check whether that APR is fixed or variable.

This detail matters because two loans can start with similar costs but behave very differently over time.

A fixed APR usually stays the same during the loan term. A variable APR can change based on market conditions, lender rules, or an index rate.

What Is a Fixed APR?

A fixed APR means the annual borrowing cost stays the same for the agreed repayment period.

If you accept a loan with a fixed APR, your rate should not suddenly increase because market rates changed later.

This can make budgeting easier because the borrower has more predictability.

- More stable monthly payments;

- Easier long-term planning;

- Lower surprise risk;

- Useful for borrowers who want predictable repayment.

What Is a Variable APR?

A variable APR can move up or down after the loan or credit product is opened.

Variable APRs are more common in credit cards, lines of credit, and some lending products. They may be tied to benchmark rates or market conditions.

The risky part is simple: the offer may look affordable today, but the cost can increase later.

Fixed vs Variable APR: Simple Comparison

| Feature | Fixed APR | Variable APR |

|---|---|---|

| Rate stability | Usually stays the same | Can change over time |

| Budgeting | Easier to predict | Less predictable |

| Risk | Lower rate-change risk | Higher rate-change risk |

| Best for | Borrowers who want stability | Borrowers who understand rate movement risk |

Why Fixed APR Usually Feels Safer for Personal Loans

For many personal loan borrowers, fixed APR feels safer because the repayment plan is easier to understand.

If I were borrowing money for a specific purpose, like debt consolidation, car repairs, medical bills, or emergency expenses, I would usually prefer knowing the payment structure before signing.

That does not automatically mean every fixed APR loan is cheap. A fixed APR can still be high. But at least the borrower has more clarity.

When Variable APR Can Become Risky

Variable APR becomes risky when the borrower only looks at the starting rate.

A loan or credit product may begin with an attractive APR, but if that APR increases later, the monthly cost can become harder to manage.

This matters especially for people already dealing with tight budgets, bad credit, unstable income, or emergency borrowing situations.

A Simple Example

Imagine two credit offers:

- Offer A: Fixed APR of 14%.

- Offer B: Variable APR starting at 12%.

At first, Offer B looks cheaper.

But if the variable APR rises later, Offer B may become more expensive than Offer A.

This is why I do not judge a loan only by the first number shown on the page.

What Borrowers Often Miss

After studying loan searches and financial comparison behavior, I noticed that many people search for speed first and cost second.

They type things like fast loan approval, emergency loan online, or loan with bad credit, but they may not stop to ask whether the APR is fixed or variable.

That missing detail can affect the entire repayment experience.

Questions I Would Ask Before Accepting Any APR

- Is the APR fixed or variable?

- If it is variable, what can make it change?

- How often can the APR change?

- Is there a maximum APR cap?

- What is the total repayment amount?

- Are there origination fees or late fees?

- Can I repay early without a penalty?

These questions help reveal whether the offer is truly manageable or just attractive at first glance.

Fixed APR and Bad Credit Borrowers

Borrowers with lower credit scores may receive higher APR offers. That is already expensive enough.

In that situation, taking on variable APR risk can make the decision even more complicated.

Before accepting any high APR loan, I would compare safer alternatives such as credit unions, smaller loan amounts, payment plans, secured options, or local assistance programs.

How I Personally Compare Fixed and Variable APR Offers

When I compare borrowing options, I try to separate the marketing from the math.

I ask myself:

- Which offer is more predictable?

- Which offer has the lower total repayment cost?

- Which one exposes the borrower to more risk?

- Is the lower starting APR worth the uncertainty?

Most of the time, predictability matters more than a slightly lower starting number.

Red Flags to Watch For

- The lender does not clearly explain whether the APR is fixed or variable.

- The offer focuses only on fast approval.

- The payment looks low but the repayment term is long.

- Fees are difficult to understand.

- The APR can change but the limits are unclear.

If those signs appear, I would slow down before applying.

Frequently Asked Questions About Fixed vs Variable APR

Is fixed APR always better?

Not always, but it is usually easier to understand and budget for because the rate is more predictable.

Can variable APR go down?

Yes, variable APR can move down in some cases, but it can also increase. That uncertainty is the main risk.

Which APR type is better for personal loans?

Many borrowers prefer fixed APR for personal loans because it provides clearer repayment expectations.

Final Guidance: Choose the APR You Can Understand

Fixed vs variable APR is not just a technical detail. It can affect your monthly payment, your total cost, and your financial stress during repayment.

If I were choosing between loan offers, I would not chase the lowest starting number blindly. I would compare APR type, total repayment cost, fees, lender credibility, and safer alternatives.

A loan should solve a problem, not create a bigger one. Understanding whether the APR is fixed or variable is one more way to borrow with caution.

When I Would Choose a Fixed APR

If I needed a personal loan for debt consolidation, home repairs, medical expenses, or another planned expense, I would usually prefer a fixed APR.

The reason is simple: I would know exactly what to expect throughout the repayment period.

When a Variable APR Might Make Sense

Variable APR products can make sense in certain situations, particularly when rates are low and the borrower expects to repay the balance quickly.

However, borrowers should understand that future rate increases can change the overall cost.

A Real Comparison Scenario

Imagine a borrower choosing between a fixed APR personal loan and a variable APR credit product.

If interest rates rise over the next two years, the variable option could become significantly more expensive. The fixed APR borrower would not face that uncertainty.

This is why many borrowers prefer paying for predictability rather than chasing the lowest starting rate.

What I Learned After Analyzing Loan Searches in Two Different Countries

Something I noticed while working on financial websites is that most borrowers never search for "fixed APR" or "variable APR". They search for things like emergency loan, fast approval, same day loan, or money now.

The funny part is that many of the long-term borrowing mistakes happen because people skip understanding how APR works altogether.

By the time they discover whether the APR is fixed or variable, they have often already focused on approval speed instead of borrowing costs.

Why I Pay Attention to APR Before Looking at Loan Marketing

Over the years I have reviewed thousands of loan-related pages, lender offers, and financial searches. One pattern appears constantly.

The marketing focuses on approval. The borrower focuses on urgency. Meanwhile, the actual borrowing cost receives far less attention.

This is why APR type is one of the first things I check when evaluating a loan.