How Personal Loans Work

How Personal Loans Work: learn how personal loans are approved, how repayment works, what APR and fees mean, and what to compare before borrowing money.

How Personal Loans Work

Personal Loans Look Simple, but the Details Matter

When someone searches for a personal loan, they usually want a clear answer fast: how much can I borrow, how quickly can I get approved, and how much will I pay every month?

I understand that urgency. After studying loan searches and financial comparison behavior, I noticed that most people do not start by asking about APR, fees, repayment terms, or total cost. They start by looking for a solution.

But that is exactly why understanding how personal loans work matters. A personal loan can help solve a short-term problem, but if the borrower ignores the terms, it can also create a longer financial problem.

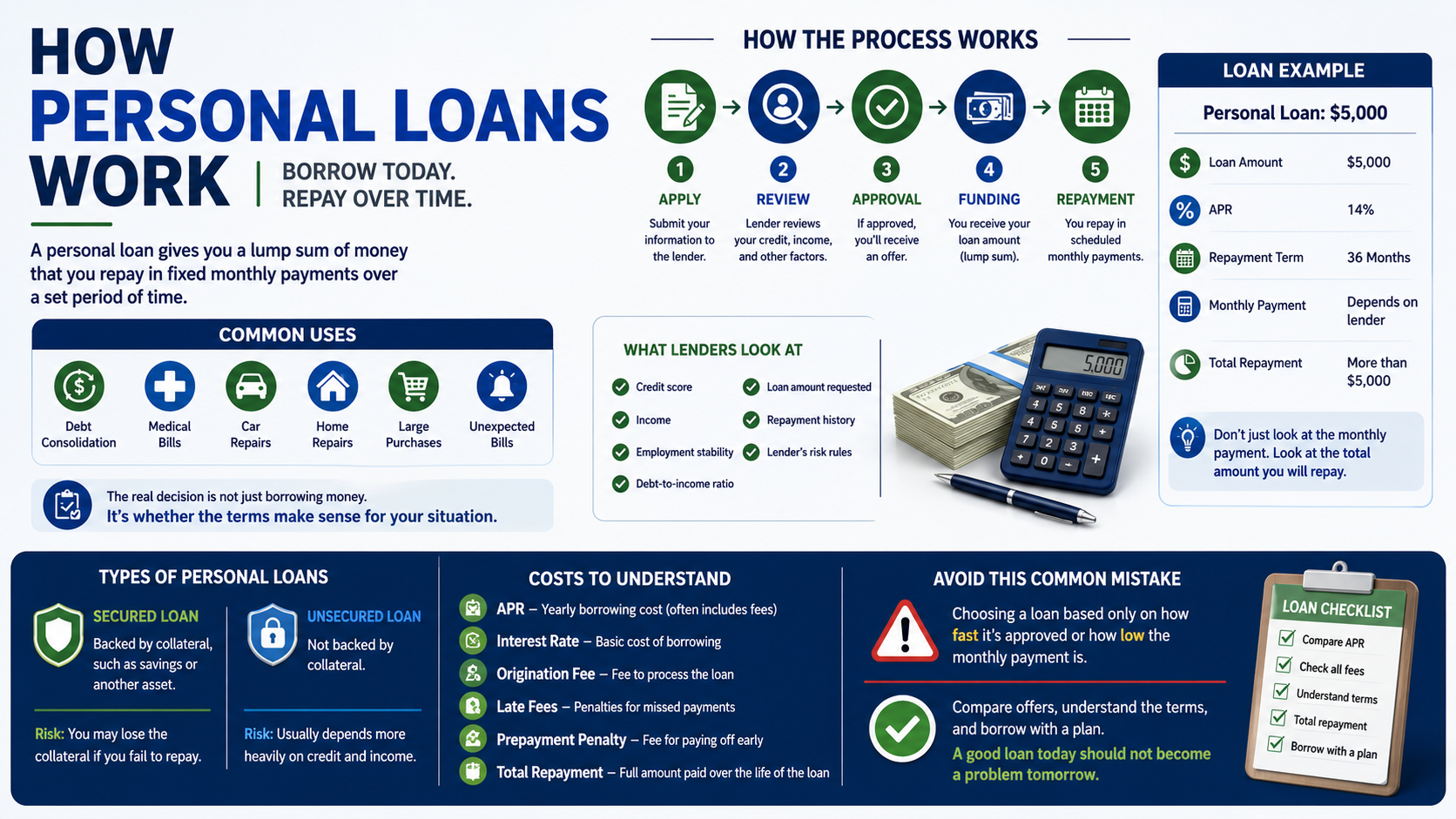

What Is a Personal Loan?

A personal loan is money borrowed from a lender and repaid over time through scheduled payments.

Most personal loans are installment loans, which means the borrower receives a lump sum and pays it back in fixed payments over a specific period.

People often use personal loans for things like:

- Debt consolidation;

- Emergency expenses;

- Medical bills;

- Car repairs;

- Home repairs;

- Large purchases;

- Unexpected bills.

The loan may feel simple at first, but the real decision is not just borrowing money. The real decision is whether the repayment terms make sense for your situation.

How Personal Loan Approval Usually Works

When you apply for a personal loan, the lender usually reviews several factors before deciding whether to approve you.

- Your credit score;

- Your income;

- Your employment or income stability;

- Your debt-to-income ratio;

- The loan amount requested;

- Your repayment history;

- The lender’s own risk rules.

This is why two people can apply for the same loan amount and receive completely different offers.

One borrower may receive a lower APR because they look less risky to the lender. Another borrower may receive a higher APR because of bad credit, unstable income, or existing debt.

How Repayment Works

After a personal loan is approved and funded, repayment usually begins according to the schedule in the loan agreement.

Most personal loans use monthly payments. Each payment may include part of the borrowed amount plus interest and, depending on the loan, certain fees.

The repayment term can vary. A shorter term may mean higher monthly payments but lower total cost. A longer term may reduce the monthly payment but increase the total amount paid over time.

A Simple Personal Loan Example

Imagine a borrower takes a $5,000 personal loan.

- Loan amount: $5,000

- APR: 14%

- Repayment term: 36 months

- Monthly payment: depends on the lender’s exact calculation

At first, the borrower may only look at the monthly payment. But the smarter question is: how much will I pay in total by the end of the loan?

That total repayment amount is what helps show whether the loan is truly manageable.

Personal Loan Costs You Should Understand

A personal loan can include more costs than the borrowed amount itself.

Before accepting any offer, I would look carefully at:

- APR: the yearly borrowing cost, often including interest and certain fees;

- Interest rate: the basic cost of borrowing the money;

- Origination fee: a fee some lenders charge to process the loan;

- Late payment fees: penalties if payments are missed or delayed;

- Prepayment penalty: a fee some lenders may charge if you repay early;

- Total repayment amount: the full amount paid over the life of the loan.

If these numbers are not clear, I would slow down before applying.

Secured vs Unsecured Personal Loans

Personal loans can be secured or unsecured.

| Loan Type | How It Works | Main Risk |

|---|---|---|

| Secured Personal Loan | Backed by collateral, such as savings or another asset | You may lose the collateral if you fail to repay |

| Unsecured Personal Loan | Not backed by collateral | Usually depends more heavily on credit and income |

Unsecured personal loans are common, but secured options may sometimes be available for borrowers who need different approval conditions.

The Common Mistake First-Time Borrowers Make

The biggest mistake I see is treating approval as the finish line.

Approval feels good, especially when someone needs money urgently. But approval does not automatically mean the loan is affordable, safe, or smart.

A borrower still needs to compare APR, fees, repayment length, total cost, and alternatives before accepting the money.

What I Learned From Studying Personal Loan Searches

While building financial content and studying loan-related searches, I noticed a pattern: borrowers often search with urgency, not patience.

They search for terms like fast personal loan, emergency loan, same day loan, loan with bad credit, or how to get approved quickly.

That urgency is real. But it can push the most important details into the background. APR, fees, repayment terms, and lender credibility matter most when the borrower feels pressured to decide quickly.

How I Personally Compare Personal Loan Offers

When I compare personal loan offers, I try to separate the marketing from the math.

My process is simple:

- First, I check the loan amount.

- Then I check the APR.

- Then I review fees and repayment terms.

- Then I compare the total repayment amount.

- Only after that do I look at the monthly payment.

- Finally, I ask if there is a safer alternative.

This helps avoid choosing a loan just because it looks fast or easy.

When a Personal Loan Can Make Sense

A personal loan may make sense when the borrower understands the cost and has a realistic plan to repay it.

Examples may include:

- Consolidating higher-interest debt;

- Covering a necessary emergency expense;

- Paying for urgent repairs;

- Replacing a more expensive borrowing option;

- Managing a planned expense with predictable payments.

Even then, the loan should fit the budget. If the monthly payment creates new financial stress, the loan may not be the right solution.

When a Personal Loan Can Be a Bad Idea

A personal loan can become risky when it is used to delay a deeper financial problem.

I would be careful if the loan is being used to:

- Pay for non-essential spending;

- Cover another loan without reducing total debt;

- Maintain a lifestyle that income cannot support;

- Borrow more than necessary;

- Accept a high APR without comparing alternatives.

A loan should solve a problem, not hide it for a few more months.

Better Alternatives Before Taking a Personal Loan

Before accepting a personal loan, I would consider whether another option could solve the problem with less risk.

- Negotiating a payment plan with the company you owe;

- Checking a local credit union;

- Borrowing a smaller amount;

- Using emergency savings if available;

- Delaying a non-urgent expense;

- Looking for nonprofit credit counseling;

- Comparing multiple lenders before applying.

The best decision is not always the fastest decision.

Red Flags Before Accepting a Personal Loan

- The lender promises guaranteed approval without reviewing your situation.

- The APR or fees are difficult to find.

- The offer focuses only on speed.

- The repayment terms are unclear.

- The lender pressures you to act immediately.

- The total repayment amount is not shown clearly.

If I see those signs, I would pause and compare other options before moving forward.

Frequently Asked Questions About How Personal Loans Work

Do personal loans affect credit score?

They can. Applying for a loan may involve a credit check, and repayment behavior can affect your credit history. Paying on time may help, while missed payments can hurt.

Can I get a personal loan with bad credit?

It may be possible, but offers may come with higher APRs, stricter terms, or smaller loan amounts. Comparing alternatives becomes especially important.

Is a personal loan better than a credit card?

It depends on the APR, fees, repayment plan, and how the money will be used. A personal loan may offer predictable payments, while credit cards can become expensive if balances remain unpaid.

Final Guidance: Understand the Loan Before You Accept the Money

Personal loans work by giving borrowers access to money now and requiring repayment over time. That sounds simple, but the details can change everything.

If I were choosing a personal loan, I would not focus only on approval speed or monthly payment. I would compare APR, fees, repayment terms, total cost, lender credibility, and safer alternatives.

The goal is not just to get approved. The goal is to borrow in a way that does not create a bigger financial problem later.

A Situation Where I Would Probably Avoid a Personal Loan

One thing I learned while researching borrowing behavior is that not every financial problem should be solved with a loan.

If someone is already struggling to make minimum payments, has unstable income, and is considering a new loan simply to cover another loan payment, I would be extremely cautious.

In that situation, borrowing more money may temporarily relieve pressure, but it may also increase the total debt burden.

Sometimes the better question is not "Can I get approved?" but "Will this loan actually improve my situation six months from now?"

A Real Comparison Process I Use When Reviewing Loan Offers

Whenever I compare personal loan offers, I create a simple checklist.

- APR

- Total repayment amount

- Origination fees

- Monthly payment

- Repayment length

- Lender reputation

What surprises many borrowers is that the lender with the lowest monthly payment is not always the cheapest option.

A longer repayment period can reduce monthly costs while increasing the total amount paid over the life of the loan.

What Most Loan Advertisements Do Not Emphasize

Loan advertisements often focus on speed, convenience, and approval odds.

Those things matter, especially during emergencies. However, what often receives less attention is the total borrowing cost.

Before accepting any offer, I believe borrowers should understand:

- How much they will repay in total;

- Whether the APR is fixed or variable;

- Whether fees are deducted from the funded amount;

- Whether early repayment penalties exist;

- How the loan fits into their monthly budget.

These details can have a bigger impact than the approval decision itself.

Questions I Would Ask Before Signing Any Loan Agreement

Before signing a loan contract, I would personally want answers to these questions:

- What is the APR?

- What is the total repayment amount?

- Are there origination fees?

- Can payments increase in the future?

- What happens if a payment is late?

- Can I repay early without penalties?

- Is this loan solving the problem or delaying it?

Asking these questions can prevent expensive surprises later.

What Building Financial Content Taught Me About Borrowing Decisions

One pattern I continue to notice is that people rarely search for loans when everything is going well financially.

Most searches happen during stressful situations: unexpected bills, emergency expenses, debt pressure, repairs, or sudden cash shortages.

Because of that, loan decisions are often emotional decisions first and financial decisions second.

That is one reason I focus so heavily on comparison, APR, repayment terms, and alternatives. A borrower under pressure is exactly the person who benefits most from slowing down and reviewing the numbers carefully.

The Most Important Takeaway

If there is one lesson I would share with someone researching personal loans, it is this:

Approval is not the goal.

The goal is finding a borrowing option that solves the problem without creating a larger one later.

That means understanding the APR, comparing alternatives, reviewing repayment terms, and making sure the loan fits your financial reality before signing anything.

A Real Scenario Where a Personal Loan Can Help

Imagine someone whose car suddenly breaks down. The repair costs $2,000, and without the vehicle, getting to work becomes difficult. In that situation, a personal loan may help solve a genuine problem that could otherwise affect income.

However, even in emergencies, I would still compare multiple offers. A loan that solves today's problem should not create a larger financial burden over the next three years.

The key question is not whether the loan can help today. The key question is whether repayment will remain manageable next month, six months from now, and next year.

What I Notice Most Often When People Search for Loans

One thing I have observed while studying loan-related searches is that most borrowers are not searching because they are excited about borrowing money.

Usually, they are facing pressure. Unexpected bills, debt, repairs, medical expenses, or temporary cash shortages are common reasons behind these searches.

Because of that pressure, many people focus on approval speed instead of loan quality. That is completely understandable, but it is also where expensive mistakes often begin.

The Difference Between Getting Approved and Choosing the Right Loan

Many borrowers treat approval as the goal.

In reality, approval is only one step in the process. The more important decision is whether the loan itself is appropriate for your financial situation.

I have seen loan offers that looked attractive because approval seemed easy, but after reviewing APR, fees, and repayment costs, the offer became much less appealing.

A smart borrowing decision requires looking beyond the approval message.

A Personal Loan Checklist I Would Use Before Applying

Before submitting any application, I would review the following checklist:

- Do I actually need to borrow this amount?

- Can I comfortably afford the monthly payment?

- Have I compared multiple lenders?

- Do I understand the APR?

- Do I know the total repayment amount?

- Have I reviewed alternative solutions?

- Am I borrowing because of a temporary emergency or a recurring problem?

These questions can often reveal issues before a borrower commits to a loan agreement.

What Responsible Borrowing Really Means

Responsible borrowing is not about avoiding loans completely. Loans can be useful financial tools when used correctly.

Responsible borrowing means understanding the costs, knowing the repayment obligations, comparing alternatives, and borrowing only what is necessary.

The strongest loan decision is often the one made after careful comparison rather than urgency.

My Final Observation After Researching Loan Comparisons

After spending years analyzing financial content and loan-related searches, one lesson continues to stand out: borrowers who understand the numbers usually make better decisions.

APR, fees, repayment terms, and total borrowing costs may not be the most exciting parts of a loan offer, but they are often the most important.

The more time you spend understanding how a personal loan works before signing, the less likely you are to face unpleasant surprises later.

Personal Loan vs Credit Card vs Payment Plan

| Option | Best For | Main Risk |

|---|---|---|

| Personal Loan | Fixed repayment structure | Long-term debt |

| Credit Card | Short-term expenses | High revolving interest |

| Payment Plan | Existing bills | Limited flexibility |