How Credit Score Affects Personal Loan Approval

How Credit Score Affects Personal Loan Approval: Learn how credit scores influence loan decisions, approval chances, interest rates, and what you can do to improve your financial profile.

How Credit Score Affects Personal Loan Approval

Why Credit Score Is One of the First Things Lenders Check

When I look at how personal loan decisions are made, one thing becomes obvious very quickly: credit score is usually the first filter.

Lenders don’t start by looking at your story or situation. They start with a number that summarizes your credit behavior over time.

That number helps them decide if it is worth analyzing your application in detail or rejecting it early.

What a Credit Score Actually Represents

A credit score is a statistical representation of your borrowing behavior. It is built from payment history, credit utilization, account age, and recent credit activity.

In simple terms, it answers one question: how likely are you to repay borrowed money on time?

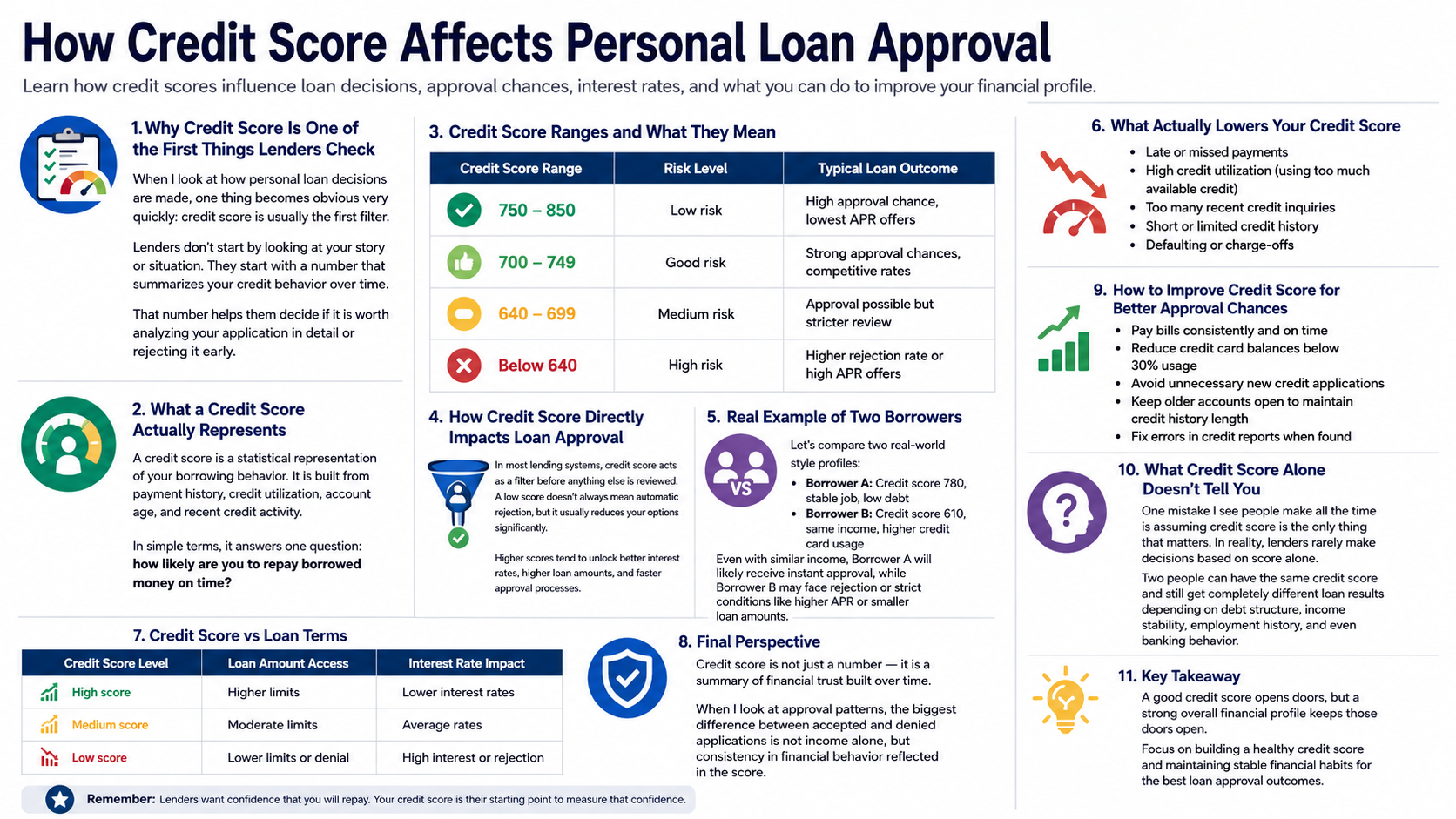

Credit Score Ranges and What They Mean

| Credit Score Range | Risk Level | Typical Loan Outcome |

|---|---|---|

| 750 – 850 | Low risk | High approval chance, lowest APR offers |

| 700 – 749 | Good risk | Strong approval chances, competitive rates |

| 640 – 699 | Medium risk | Approval possible but stricter review |

| Below 640 | High risk | Higher rejection rate or high APR offers |

How Credit Score Directly Impacts Loan Approval

In most lending systems, credit score acts as a filter before anything else is reviewed. A low score doesn’t always mean automatic rejection, but it usually reduces your options significantly.

Higher scores tend to unlock better interest rates, higher loan amounts, and faster approval processes.

Real Example of Two Borrowers

Let’s compare two real-world style profiles:

- Borrower A: Credit score 780, stable job, low debt

- Borrower B: Credit score 610, same income, higher credit card usage

Even with similar income, Borrower A will likely receive instant approval, while Borrower B may face rejection or strict conditions like higher APR or smaller loan amounts.

What Actually Lowers Your Credit Score

- Late or missed payments

- High credit utilization (using too much available credit)

- Too many recent credit inquiries

- Short or limited credit history

- Defaulting or charge-offs

One Insight Most People Don’t Realize

From analyzing lending patterns, I noticed something important: credit score alone is not the full story.

Two people with the same score can get different results depending on debt structure and income stability. Lenders often combine credit score with debt-to-income ratio before making a final decision.

How to Improve Credit Score for Better Approval Chances

- Pay bills consistently and on time

- Reduce credit card balances below 30% usage

- Avoid unnecessary new credit applications

- Keep older accounts open to maintain credit history length

- Fix errors in credit reports when found

Credit Score vs Loan Terms

| Credit Score Level | Loan Amount Access | Interest Rate Impact |

|---|---|---|

| High score | Higher limits | Lower interest rates |

| Medium score | Moderate limits | Average rates |

| Low score | Lower limits or denial | High interest or rejection |

Final Perspective

Credit score is not just a number — it is a summary of financial trust built over time.

When I look at approval patterns, the biggest difference between accepted and denied applications is not income alone, but consistency in financial behavior reflected in the score.

What Credit Score Alone Doesn’t Tell You

One mistake I see people make all the time is assuming credit score is the only thing that matters. In reality, lenders rarely make decisions based on score alone.

Two people can have the same credit score and still get completely different loan results depending on debt structure, income stability, and recent credit activity.

The Hidden Factor: Credit Utilization

Credit utilization is one of the most underestimated parts of your credit profile. It measures how much of your available credit you are actually using.

Even if your score looks “good,” high utilization (above 30–40%) can still trigger higher interest rates or rejection in stricter lenders.

Realistic Borrower Scenario (Based on Lending Patterns)

Let’s take a more realistic case than simple textbook examples:

- Borrower A: Credit score 720, 25% credit utilization, stable income

- Borrower B: Credit score 740, 65% credit utilization, frequent new credit inquiries

Even though Borrower B has a higher score, many lenders still prefer Borrower A because their credit behavior looks more stable and predictable.

Comparison: What Actually Impacts Loan Approval Most

| Factor | Impact Level | Why It Matters |

|---|---|---|

| Credit Score | High | Quick risk screening |

| Credit Utilization | Very High | Shows financial pressure |

| Debt-to-Income Ratio | Very High | Repayment capacity |

| Income Stability | High | Predictability of payments |

A Mistake Most Borrowers Don’t Realize They Are Making

Something I’ve seen repeatedly is people applying for loans right after checking offers from multiple lenders in a short period.

Each application can generate a hard inquiry, and too many of them close together can signal financial stress — even if your credit score is strong.

A More Human View of Credit Decisions

One thing I learned analyzing real loan outcomes is that credit scoring systems are not as clean as people think. They are statistical models, not perfect judgments.

I’ve seen cases where applicants with solid scores still got denied simply because their credit activity changed too quickly in a short period of time.

It’s not always about “good or bad credit” — it’s about timing, stability, and how predictable your financial behavior looks at that moment.

A Realistic Case That Shows How It Works in Practice

Imagine two applicants applying for the same $5,000 personal loan:

- Applicant A: stable credit history, low credit usage, no recent new accounts

- Applicant B: similar score, but opened 3 new credit accounts in the last 60 days

Even with almost identical credit scores, Applicant A is usually seen as lower risk because their behavior is more stable and predictable from a lender’s perspective.

What Most People Misunderstand About Loan Approval

A common assumption is that improving your credit score alone guarantees better loan approval chances. In reality, lenders look at patterns, not just numbers.

Things like recent credit activity, utilization spikes, or unstable income can weigh just as heavily as the score itself.

Final Thought

Credit score is useful, but it’s only one part of the decision-making process.

If there’s one takeaway from analyzing lending behavior, it’s this: consistency over time matters more than short-term improvements.

That’s what lenders ultimately reward — predictable financial behavior, not just high numbers.