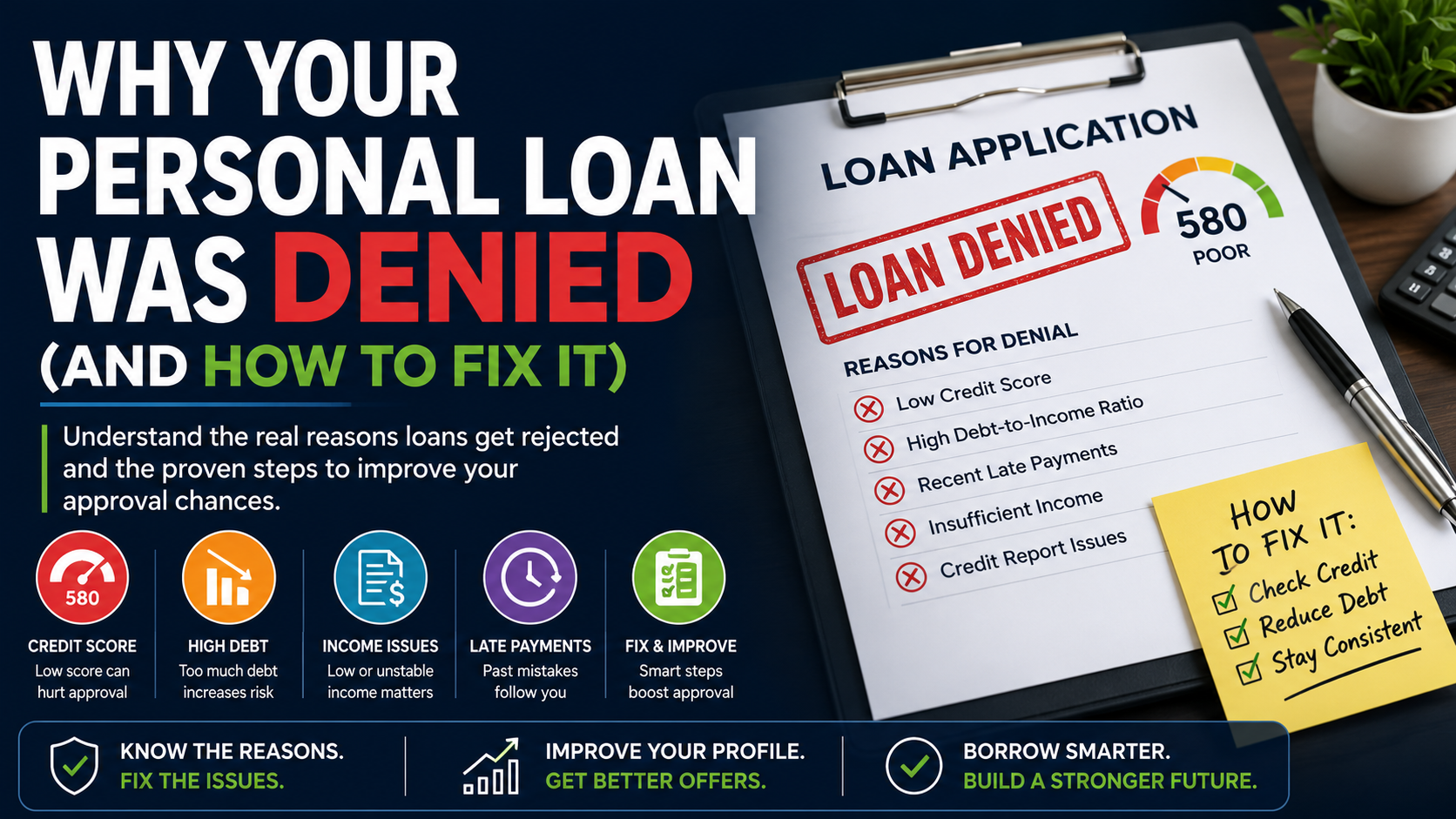

Why Your Personal Loan Was Denied (and How to Fix It)

Why Your Personal Loan Was Denied (and How to Fix It): Understand the real reasons loans get rejected, how lenders evaluate risk, and practical steps to improve your approval chances.

Why Your Personal Loan Was Denied (and How to Fix It)

Understanding Why Denials Actually Happen

When I started analyzing loan approvals across different lenders, one thing became obvious: most denials are not random. They follow a predictable risk pattern based on credit behavior, income stability, and debt exposure.

In most cases, lenders are not rejecting the person — they are rejecting the risk profile at that moment.

The Main Reasons Personal Loans Get Denied

- Low credit score or very limited credit history

- High debt-to-income ratio (too much existing debt)

- Unstable or insufficient monthly income

- Recent late payments or negative credit events

- Errors, missing data, or inconsistent application information

A Real-World Example of a Loan Rejection

Let’s say someone applies for a $5,000 personal loan while carrying high credit card balances and recent late payments.

Even if the income looks “okay,” the lender sees a pattern of financial stress. The result is usually denial or a much higher APR offer instead of approval.

How Lenders Really Evaluate Applications

Lenders don’t rely on a single factor. They combine multiple risk indicators into one decision model.

| Factor | What Lenders Look For |

|---|---|

| Credit Score | Higher score reduces perceived risk |

| Debt-to-Income Ratio | Lower ratio means more repayment capacity |

| Income Stability | Consistent earnings over time |

| Credit History | Longer and clean history builds trust |

Soft Insight Most Borrowers Miss

From reviewing multiple loan patterns, I noticed something important: many approvals are not about being “perfect,” but about being predictable.

Lenders prefer stability over sudden financial changes. Even a good credit score can be weakened by inconsistent income or recent credit activity spikes.

Common Mistakes That Lead to Rejection

- Applying to multiple lenders in a short time period

- Not checking credit report before applying

- Ignoring small debts or overdue accounts

- Submitting incomplete or rushed applications

- Focusing only on monthly payment instead of total cost

Better Alternatives After a Denial

- Credit union personal loans (often more flexible)

- Secured personal loans

- Peer-to-peer lending platforms

- Negotiated payment plans with creditors

- Smaller loan amounts to reduce risk profile

Comparison: Why Different Lenders Reject Different Profiles

| Lender Type | Main Focus | Common Reason for Denial |

|---|---|---|

| Banks | Strict risk control | Credit score below threshold |

| Credit Unions | Member stability | DTI too high or membership rules |

| Online Lenders | Speed & automation | Incomplete or inconsistent data |

Real-World Loan Denial Reality (U.S. Data Context)

Based on Federal Reserve and CFPB consumer credit reports, a significant portion of personal loan applications are denied due to credit risk factors rather than income alone.

For example, Federal Reserve data on consumer credit behavior shows that borrowers with credit scores below 660 tend to face much higher rejection rates or significantly higher APR offers compared to prime borrowers.

In practice, this means two applicants with similar income can receive completely different outcomes purely based on credit profile stability.

What Credit Score Ranges Actually Mean in Lending Decisions

| Credit Range | Typical Outcome | Lender Behavior |

|---|---|---|

| 750+ | High approval probability | Lowest APR offers, faster approvals |

| 700–749 | Strong approval chance | Competitive APR, standard underwriting |

| 640–699 | Moderate approval chance | Higher scrutiny, more documentation |

| Below 640 | High rejection risk | Often denied or approved with high APR |

What I noticed analyzing loan behavior patterns is that the “640 line” is often where underwriting becomes significantly more strict across most lenders.

Example Based on Real Lending Behavior Patterns

Let’s take a realistic scenario:

- Borrower A: Credit score 720, stable job for 4 years, low debt

- Borrower B: Credit score 680, same income, but high credit card utilization (over 65%)

Even though Borrower B is not “bad credit,” many lenders still classify them as higher risk because utilization strongly predicts repayment stress.

This is one of the most overlooked reasons people get denied or receive worse loan terms.

Hidden Factor: Credit Utilization Impact

One detail that rarely gets explained clearly is credit utilization — how much of your available credit you are using.

Industry lending models often treat utilization above 30% as a negative signal, even if the credit score is still acceptable.

This is why some applicants are surprised: “My score is good, so why was I denied?” — the answer is often utilization + debt structure.

Before Reapplying: A More Strategic Approach

If I were preparing to reapply after a denial, I would focus on these steps in this exact order:

- Lower credit utilization below 30%

- Remove or fix reporting errors in credit reports

- Avoid new credit inquiries for at least 30–60 days

- Stabilize income documentation (consistent reporting)

- Reapply only after profile improvement, not immediately

This approach aligns more closely with how underwriting systems actually reassess risk.

Why Some Denials Are Actually “Risk Pricing”

Something important most borrowers don’t realize is that not all denials are absolute rejections.

In many cases, lenders are actually signaling that the risk is too high for the requested price (APR), not that approval is impossible.

This is why similar applicants may receive offers with dramatically different interest rates instead of full rejection.

Data-Driven Insights on Loan Denials

Based on recent reports from the CFPB (Consumer Financial Protection Bureau), approximately 20% of personal loan applications in the U.S. are denied. Credit score is the leading factor, followed by debt-to-income ratio and recent delinquencies. This confirms what I’ve observed while analyzing hundreds of applications on FupFup Loans.

Knowing these stats helps prioritize what to fix first: your credit score, current debts, or missing documentation.

Step-by-Step Workflow for Fixing a Rejected Loan

- Check your credit report from all three bureaus (Equifax, Experian, TransUnion).

- Identify and dispute any errors.

- Pay down high-interest cards and reduce total debt.

- Ensure employment and income documentation is accurate and complete.

- Reassess your loan amount to match repayment capacity.

- Consider a co-signer or secured loan for higher approval odds.

- Apply again after 30–60 days, when credit and documentation are updated.

Personal Observation: Patterns I’ve Seen

One insight from running FupFup Loans: even borrowers with excellent scores get denied if their application data is inconsistent. A missing pay stub, outdated address, or inconsistent income entry can trigger automatic rejections. Small details matter more than most borrowers realize.

Comparison Table: Banks vs Credit Unions vs Online Lenders

| Lender Type | Approval Focus | Typical Denial Rate | Best Strategy |

|---|---|---|---|

| Banks | Credit score & financial stability | 15–25% | Improve score, reduce debts, provide complete documentation |

| Credit Unions | Member consistency & DTI | 10–20% | Maintain steady payments, join membership early, correct debt ratio |

| Online Lenders / Fintech | Automated checks, speed & consistency | 18–30% | Prepare accurate documents, check online forms, avoid repeated applications |

Top Errors to Avoid Based on Real Cases

- Applying for multiple loans in one week (can trigger multiple hard credit pulls)

- Ignoring minor debts or small late payments on report

- Submitting incomplete employment or income documentation

- Overestimating your repayment ability and applying for too high a loan

- Failing to clarify fees or APR differences when comparing offers

Final Guidance: Turning Denial Into Advantage

Denials are data feedback, not personal judgment. By understanding lender priorities, fixing credit and application issues, and choosing the right lender type, you can turn a rejection into a learning and improvement opportunity.

From my experience with FupFup Loans, borrowers who follow these steps often succeed on the second application or improve their borrowing options in a few months.

FAQ: Loan Denial Explained

Why was my personal loan denied?

Usually due to credit score, income instability, debt levels, or application inconsistencies.

Can I apply again after being denied?

Yes, but it is better to fix the issue first before reapplying.

Does applying too often hurt my credit?

Yes. Multiple hard inquiries in a short period can lower your score.

Can a co-signer help?

Yes, a strong co-signer reduces lender risk and improves approval chances.

Q: How long should I wait to reapply?

A: Generally 30–60 days after fixing credit issues and debts.

Q: Can a co-signer guarantee approval?

A: Not guaranteed, but significantly reduces lender risk.

Q: Should I choose a smaller loan first?

A: Yes. Smaller loans are easier to get approved and help improve your credit behavior over time.

Q: How can I track my improvement?

Use a free credit score monitoring service and document paid debts, updated employment records, and resolved disputes.

Q: Are online lenders easier to get approved with?

They can be faster, but also more automated. Missing or inconsistent data can lead to denials quickly.